The news space has been agog with the news of high profile individuals, politicians and businessmen, all over the world owning offshore companies in what has been dubbed the ‘Pandora Papers’. It is said to be a project involving 600 journalists from 150 news organisations around the world with a cache of 11.9 million confidential files purportedly exposing how the world super rich use tax havens to avoid paying tax. This is not the first time investigations about shell companies involving the ultra rich have made their way to the mainstream media. In 2017, a similar report tagged ‘the Paradise Papers’, a report of 1.4 terabyte data, created a sensation when it was released.

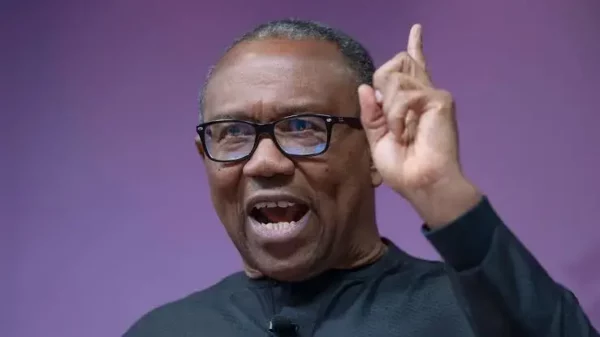

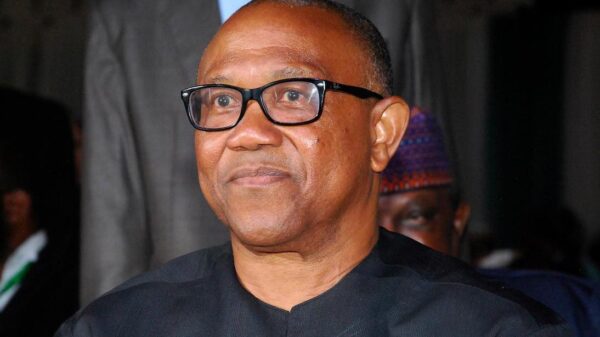

Peter Obi, a two term governor of Anambra State and former presidential aspirant under the PDP was one of the names dropped by the report. A politician known for his trailblazing policies and enviable record as a pacesetter and administrator extraordinaire. As governor, Mr. Obi’s ANIDS (Anambra Integrated Development Strategy), an initiative premised on the internationally acclaimed Millennium Development Goals (MDGs) of eradicating of extreme poverty, reduction of child mortality, boost to maternal health, environmental sustainability and global partnership in development, left behind an infrastructurally improved state. His investment in education transformed the educational system of the state, making it possible for the state to become the best performing state in mathematics and sciences, best in NECO, best in WAEC and overall best in JAMB scores.

His administration’s policies attracted direct foreign investment, which provided jobs and encouraged indigenous investments. It is on record that he left his state debt free at the end of his tenure as governor of Anambra state. Former World Bank Director in Nigeria, Omo Ruhl once described him as “an exceptional leader and very prudent in financial management and I believe his interest is to better the lots of his people which to my mind is very remarkable.”

In the light of the coming high octane drama that is Nigerian political season, it is no surprise that Mr. Obi has found himself at the center of an unwelcome attention. In the ‘Pandora Papers’, there are insinuations of illegality surrounding his ownership of offshore companies. His companies Gabriella Investment, PMGG Investment and Trust, Gabriella Settlement were entities listed in the reports. The tradition of using offshore companies is worldwide and not peculiar to Nigeria. Now it begs the question, did Mr. Obi break the law by owning these companies. In my opinion, he did not. There’s nothing unlawful in the ownership of offshore companies as long as they are not vehicles for money laundering. The report aimed through the emphasis on the listed companies, to portray the former governor and presidential aspirant as though he had committed a crime by ownership of offshore companies whereas there is no law in Nigeria stipulating ownership of offshore assets as a crime.

On the issue of failure to declare his companies assets to the Code of Conduct Bureau, Mr Obi had stated in his defense that he was not under obligation to declare companies jointly owned. A statement which the report appears to vilify. Indeed the code of conduct law requires public office holders to declare own assets, as well as those owned by their spouses and children below the age of 18. However, the report failed to show if the listed companies linked to Mr. Obi held any assets, traded or conducted business that would have generated taxable income in order to qualify as ‘assets’. If these companies, registered way before Mr. Obi became a public official are not proven to generate income, then these reports are malicious and aimed at painting Mr. Obi in a poor light.

The report also accuses Mr. Obi of owning a Lloyds TSB bank account as governor in contravention of the Code of Conduct Law, while in the same breath admitting that the account was opened in 2001, five years before he became governor. What the report should have told Nigerians is if the said account was active and used for transactions while Mr. Obi was governor.

Taking a look at the issue of declaring his family’s trust, we must look to the Personal Income Tax (Amendment) Act for guidance. It must be noted that there is a school of thought that supports the argument that only the amount distributed from an Offshore Trust to a taxable person in Nigeria will form a taxable income in Nigeria and not the entire income derived by the Offshore Trust from the assets/ investments held in trust. Such income will then be exempted from tax where it is brought into Nigeria through Government approved channels, such as the commercial banks. Now, the reports failed to showed how the Trust is administered and whether any amount is paid to Mr. Obi in order to make him liable of tax avoidance. Rather it avers that a New Zealander entity, Granite Trust Company Limited is the sole trustee of The Gabriella Settlement. Should a foreign trustee be subject to Nigerian tax laws?

Paragraph 1 of the second schedule to PITAM provides that the income of a Trust shall be deemed to be income of the Settlor of the Trust where the Settlor retains or has a right over the capital assets of the trust; retains or has a right over the income derived from the capital assets of the trust; makes use of the income of the trust by borrowing from it; and resumes control or the spouse resumes control over the asset or income of the Trust. By this submission, Granite Trust Company, a non-Nigerian entity cannot be liable to Nigerian tax laws as it is the sole trustee of the trust.

If Mr. Obi has no legal authority to either control or influence the trust, how can he be said to have broken the law? These are the pertinent questions that begs answers.

Umari Ayim is a Chartered Arbitrator & Managing Partner, Golde Aten Consultants & Solicitors

____

Follow us on Twitter at @thesignalng

Copyright 2021 SIGNAL. Permission to use portions of this article is granted provided appropriate credits are given to www.signalng.com and other relevant sources.